![Just like AIG, which was bailed out by the American Government for $180 billion, European financial institutions Société Générale, BNP Paribas, Barclays and Commerzbank hugely benefited from implicit government guarantees. ©3d-Master-AdobeStock [copyright]](/sites/default/files/styles/event_news_une/public/2019-09/IGG_1.jpg?itok=Xrzr4BVM)

In his latest published research, Professor Lei Zhao explains why and how he managed to measure the implicit government guarantees enjoyed by European financial institutions, which increased substantially during the recent financial crises. This may help devise regulations that aim to reduce the induced market distortion.

“Public subsidies have long been known to pose a serious threat to the stability of the financial system,” writes LabEx ReFi member Lei Zhao in the article he published in European Financial Management. “On the one hand, the presence of government guarantees extended to too-big-to-fail (TBTF) institutions may reduce market discipline and induce protected banks to take more risk. On the other hand, the guarantees may, through competition, push the protected banks’ competitors toward higher risk-taking.”

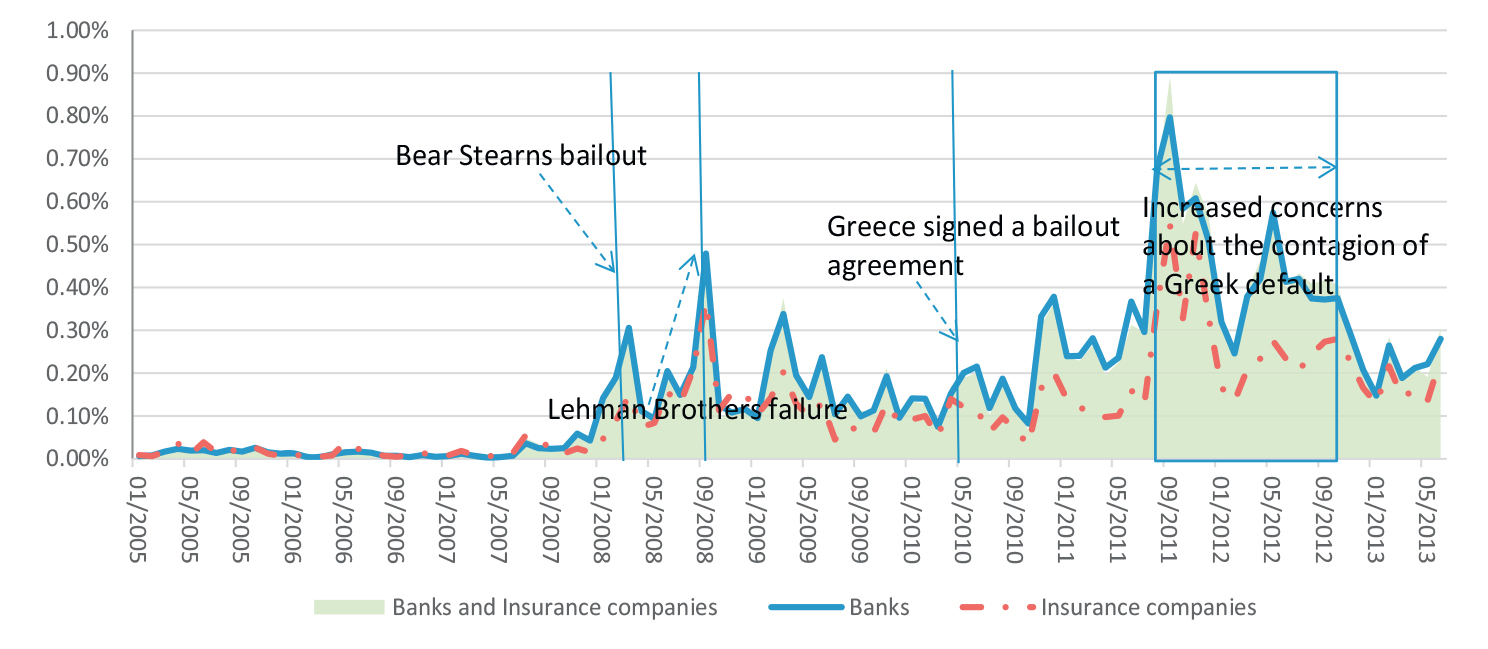

Therefore, it is important to better understand and, as a first step, measure the implicit government guarantees (IGG), which “stem from the expectation that the government will lend support to troubled financial firms that are deemed to be of systemic importance.” In his article, Lei Zhao estimated the magnitude of IGG in European financial institutions (insurance companies and banks) by exploiting the price differential of credit default swap (CDS) contracts written on debts with different levels of seniority from 2005 to 2013. He also studied the impact of new financial regulations on such guarantees. “The estimates of IGG at the firm level may help devise regulations that aim to reduce market distortion induced by such implicit support,” he explains.

The ESCP Professor of Finance determined that the aggregate guarantee increased substantially during the recent financial crises, reaching its record high in 2011 - in the heat of the European sovereign debt crisis. “During the sample period (January 2005 to June 2013), the largest financial firms (46 institutions in the sample) enjoyed an average implicit subsidy of €34 billion per year. The annualised subsidy was merely €1.83 billion before the crises and became as large as €175 billion in September 2011…”

“In addition, my finding that only a small number of large financial firms contribute to the majority of total implicit guarantees supports current policy actions directed at containing bank size,” he writes. Eight institutions remain consistently among the top 15 firms that benefit the most from IGG, including Société Générale, BNP Paribas, Barclays and Commerzbank… Interestingly, this did not prevent BNP Paribas’ Senior Economist for China from welcoming Beijing’s decision to put an end to its IGG policy for banks.

His analysis further suggests that the extent of implicit support depends on the type of institutions: banks are perceived by the CDS market to be more systemically important and thus more likely to be bailed out by the government during difficult times, leading to banks enjoying higher IGG than insurance companies. Lei Zhao’s findings confirm the presence of the “TBTF effect” in the European financial system. Such effect has real-world consequences: “The substantial implicit guarantees extended to banks and insurance companies encourage them to grow larger (i.e., to become more systemically important).”

He also showed that there exists a eurozone effect: “Within Europe, eurozone financial firms are found to enjoy more IGG than non-eurozone ones, which may raise unfair-competition issues.”

Lei Zhao further investigated the potential feedback relationship between government support and sovereign credit risk, showing that the guarantee implicitly offered by a government increases the sovereign’s default risk (a failure in the repayment of a county's government debts, which would make borrowing funds in the future more difficult and expensive). Interestingly, a major international regulatory response to the recent financial crisis, does not seem to reduce IGG: “I find that the announcement of Basel III failed to curb the perception of public support for the financial sector. It seems that the market is not convinced that the proposed regulation of TBTF institutions will be effective.”

Campuses